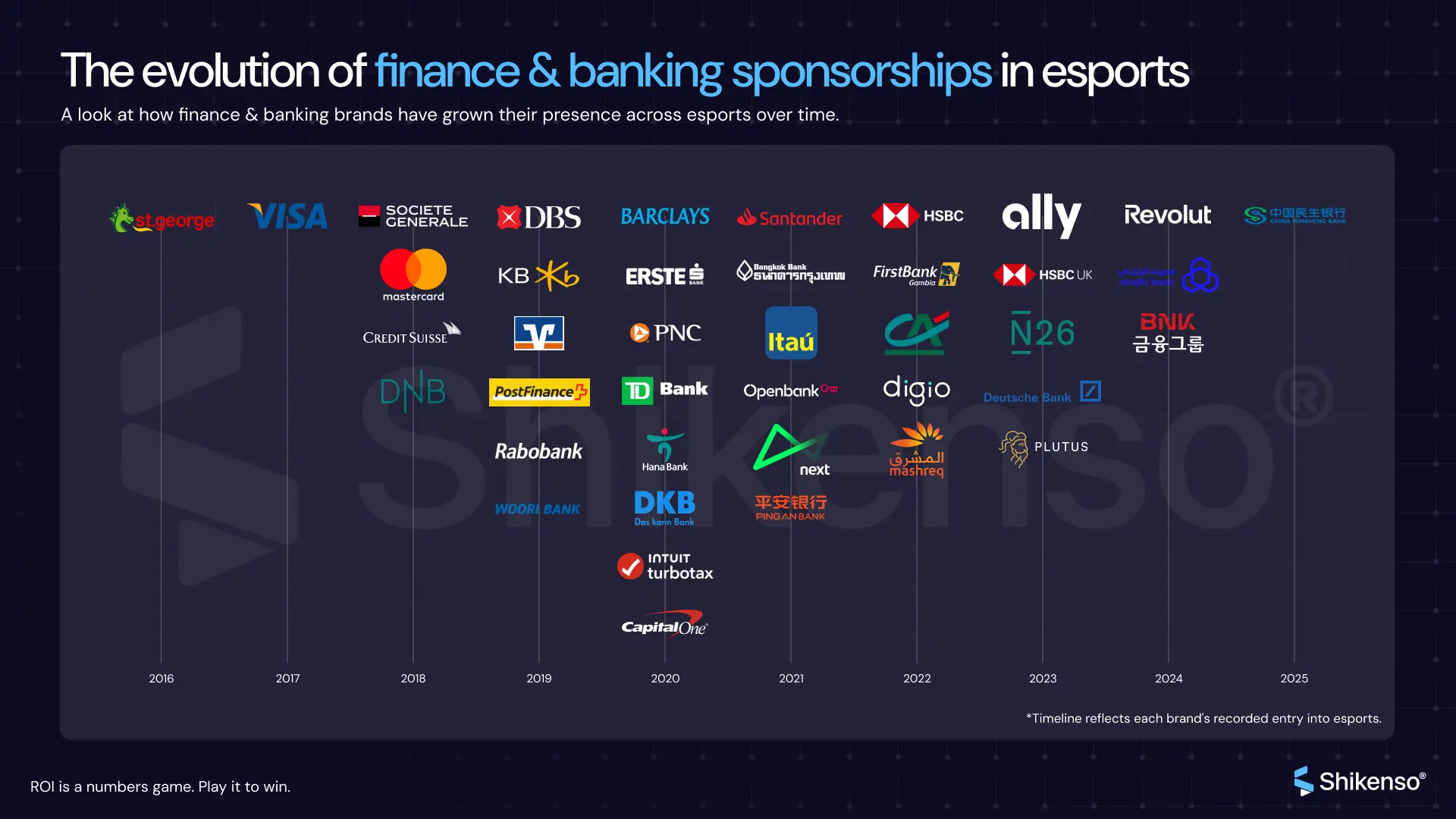

Banks don't typically rush into unproven markets. Yet between 2016 and 2026, over 20 financial institutions entered esports—from global payment processors like Visa and Mastercard to regional players like Woori Bank and Al Rajhi Bank. Some tested once. Others built decade-long commitments.

What changed? The audience. Esports demographics skew towards the 18-34 bracket—precisely the generation banks need to reach as they shift away from traditional branch banking. By 2025, the question wasn't whether banks should be in esports, but which partnerships deliver measurable brand lift and customer acquisition.

This timeline tracks a decade of finance moving into competitive gaming, from early Australian experiments to Mastercard's global League of Legends empire.

The Numbers: Who Stayed, Who Tested, Who Expanded

Between 2016 and 2026, the banking and finance sector made 30+ documented esports partnerships. Here's the breakdown:

- 3 institutions with sustained multi-year commitments: Mastercard (2018-2023+), HSBC/HSBC UK (2023-2024+), TD Bank (2020-2022+)

- 8-year gap, one brand: Visa left esports in 2017, returned in 2025 with a women's development programme

- Regional wave: 2024-2025 saw four Asian banks enter (BNK Financial Group, Al Rajhi Bank, Minsheng Bank, Woori Bank)

- Fintech's entry: Revolut became the first neobank to sponsor esports in 2024 with BLAST Premier CS2

- Multi-region simultaneous activation: Santander signed three League of Legends circuits in 2022 (LEC, LLA, CBLOL)

The pattern is clear. Traditional banks tested locally first—St. George Bank in Australia, Barclays in UK universities, PNC Bank with Pittsburgh Knights. Payment processors went global from day one. Regional banks waited until 2024-2025 to enter established markets.

Major Partnership Examples

St. George Bank x ESL Australia (2016)

St. George Bank became one of the first traditional banks to sponsor esports when they partnered with ESL Australia in 2016. The partnership covered Counter-Strike, Halo, and Hearthstone across Australia and New Zealand. This early move from a retail bank demonstrated that financial institutions could activate in competitive gaming markets outside the US and Europe, setting a precedent for regional banks worldwide.

Visa x SK Gaming (2017)

Visa partnered with SK Gaming in 2017, backing one of Europe's most established CS:GO organisations. The deal positioned Visa as a global payments partner during SK Gaming's competitive peak. However, Visa exited esports sponsorships after this partnership, not returning until 2025—an eight-year gap that reflects the cautious approach many financial institutions took during esports' volatile growth period.

Mastercard x Riot Games (2018-Present)

Mastercard signed with Riot Games in 2018, becoming the official payment services partner for League of Legends global events. The partnership renewed in 2022 and expanded to VALORANT in 2023, making Mastercard the longest-tenured financial services brand in esports with 5+ years of sustained activation.

Mastercard's integration went beyond logo placement. The brand created cardholders-only experiences at Worlds, offered exclusive merchandise, and integrated payment solutions at live events. The multi-game expansion to VALORANT showed Mastercard's confidence in Riot's portfolio and willingness to follow competitive gaming audiences across titles.

Barclays x UK Esports (2020)

Barclays made two simultaneous UK-focused entries in 2020: sponsoring the UKLC (UK League Championship) and partnering with NSE (National Student Esports) for the British University Esports Championships. This dual activation targeted both professional and grassroots competitive gaming, positioning Barclays as a supporter of UK esports infrastructure during a period of rapid domestic growth.

Santander x Riot Games Circuits (2022)

Santander executed a coordinated triple entry in 2022, sponsoring three League of Legends regional circuits simultaneously: LEC (Europe), LLA (Latin America), and CBLOL (Brazil). This multi-region strategy gave Santander presence across Riot's entire Western hemisphere competitive ecosystem in a single year, demonstrating how established banks could leverage global infrastructure to activate at scale.

Ally Financial x Rocket League (2023-2024)

US-based Ally Financial became the official automotive financing partner of Rocket League Esports (RLCS) in 2023, marking one of the few finance partnerships focused exclusively on a non-MOBA, non-FPS title. The partnership expanded in 2024 to cover both North America and Europe, showing Ally's commitment to Rocket League's unique car-focused audience demographic that aligned naturally with an automotive finance brand.

Revolut x BLAST Premier (2024)

Revolut became the first neobank and fintech company to sponsor esports when they partnered with BLAST Premier for Counter-Strike 2 in 2024. The partnership brought a digital-first financial services brand into CS2's global tournament circuit, representing a shift from traditional retail banks to fintech platforms targeting younger, digitally-native audiences.

HSBC x T1 Esports (2024)

HSBC Hong Kong partnered with T1 Esports in 2024, coinciding with T1's dominance in League of Legends during their championship run. This marked HSBC's expansion beyond their earlier UK-focused partnerships (EXCEL and GIANTX) into Asian markets, targeting Hong Kong's passionate League of Legends fanbase through one of the most successful organisations in the game's history.

Visa x DUX Gaming (2025)

After an eight-year absence, Visa returned to esports in 2025 through DUX Gaming's women's development programme, "DUX Academy powered by Visa." Rather than backing a traditional team sponsorship, Visa focused on talent development and women's competitive gaming in Spain. This strategic re-entry reflected the growing focus on diversity and grassroots investment rather than top-tier team logos.

Woori Bank x MSI 2025 & LCK (2025)

South Korea's Woori Bank entered esports by sponsoring MSI 2025's Vietnamese broadcast through VTVcab while simultaneously backing LCK (League of Legends Champions Korea) and VCT Pacific for VALORANT. This multi-game, multi-region approach gave Woori Bank presence across the two largest esports titles in Southeast Asia and Korea, targeting the core competitive gaming audience in one of the world's most mature esports markets.

Re-Entry Patterns: Which Banks Stayed Committed

Why Finance Brands Sponsor Esports

The banking and finance sector didn't enter esports for brand awareness alone. Here's what drives these partnerships:

- Demographic targeting – Esports audiences are 18-34, digitally native, and represent the next generation of banking customers. Traditional branch banking is declining; digital acquisition is critical.

- Payment integration opportunities – Mastercard and Visa didn't just sponsor—they integrated payment solutions into ticketing, merchandise, and in-game transactions at live events.

- Regional market penetration – Banks like Santander, HSBC, and Woori used esports to reach specific geographic markets (Latin America, UK/Hong Kong, Southeast Asia) where traditional advertising has diminishing returns.

- Youth brand repositioning – Institutions like Barclays and TD Bank used esports to shed "legacy" perceptions and position themselves as forward-thinking brands relevant to Gen Z.

- Measurable digital touchpoints – Unlike traditional sports, esports partnerships deliver trackable impressions through streaming platforms, social media integrations, and digital-first activations.

The 2024-2025 Regional Wave: Asian Banks Enter

While Western banks tested esports between 2016-2022, Asian financial institutions waited. Then 2024-2025 brought a coordinated wave:

- BNK Financial Group (South Korea) partnered with FEARX for League of Legends, VALORANT, and Rainbow Six

- Al Rajhi Bank (Saudi Arabia) backed Twisted Minds across multiple games

- Minsheng Bank (China) sponsored Mobile Legends: Bang Bang

- Woori Bank (South Korea) entered with MSI 2025, LCK, and VCT Pacific

This wasn't coincidence. These markets had mature esports ecosystems, proven ROI data from Western bank partnerships, and regulatory clarity around gaming sponsorships. The regional wave showed that banking's esports adoption followed infrastructure maturity, not hype cycles.

The Outliers: What Didn't Come Back

Not every bank renewed. Several institutions tested once and exited:

- St. George Bank (2016) – Australia's first mover didn't return after ESL Australia

- Societe Generale (2018) – Backed GamersOrigin in France, single partnership

- PNC Bank (2020) – Sponsored Pittsburgh Knights, no follow-up

- Revolut (2024) – BLAST Premier partnership ongoing but no expansion yet

These exits don't indicate failure—some brands achieved their objectives and reallocated budgets. Others found esports audiences didn't convert to banking customers at expected rates. The critical difference? Mastercard, HSBC, and TD Bank built multi-year strategies with measurable KPIs, while one-off partnerships lacked infrastructure for attribution and renewal justification.

A Decade of Financial Services in Competitive Gaming

The brands still active in 2026 share common traits: multi-year commitments, integration beyond logos, and measurable digital strategies. The ones that left tested without infrastructure or exited when objectives were met. What started as risky bets on an unproven audience became calculated investments in a generation that banks can't afford to ignore.

Related reads

Get new insights straight to your inbox

Don’t miss out on the insights that the press and media rave about!